On Tuesday, November 7, I’ll be recording a live podcast with Jeremy Cohen of Think Autonomous.

Jeremy was one of the earliest students in the Udacity Self-Driving Car Nanodegree Program. He now has an online education startup of his own, offering advanced courses in many of the topics key to self-driving.

RED Mountain is a gem of a ski area, set just over the border from Washington, in British Columbia. Some notes:

The area is the size of a major western US resort – it’s larger than Northstar or Steamboat Springs, and only a bit smaller than Heavenly or Breckenridge, with 20% as many skiiers.

The name of the resort refers to the iron in the mountain, rather than anything to do with communism.

Canadian ski areas close at 3pm, compared to 4pm in the US. I unknowingly caught the last lift up at 2:58pm, cruised down the back-side of the mountain and popped into a lodge. My arrival bewildered the staff to the point of annoyance, until they realized I was a confused American. They pointed me on a route to the bottom of the resort without getting stuck at some closed lift.

I think there is a “BC Curve” for ski run ratings, the same way I think Mammoth has a “Southern California Curve.” There are black runs at Mammoth that seems pretty blue to me, and there are plenty of blue runs at RED that seem pretty black to me. It’s steep.

The bar at the base has a wall featuring all the locals who’ve skiied for the Canadian National Team. The heyday seems to have been the 70s.

Most of the lifts are a little old school. One whipped around so quickly after dismounting that it clocked me in the back of the head and knocked me to the deck. Fortunately, I was wearing a helmet, so nothing was injured but my pride.

The IKON Pass doesn’t work directly, maybe because RED Mountain is independently-owned. Instead, I had to take my IKON Pass to the ticket window and scan it for a RED Mountain lift pass.

Flying Phil’s Mexican food truck serves excellent gourmet Mexican fare. If you can get over the incongruity of “gourmet Mexican food out of a truck at the bottom of a ski run in Canada”, it’s worth a stop.

The resort has cabins for rent in the middle of one of the ski runs on the middle of the mountain. $500 per night seems steep to me, even in Canadian dollars, but they look awesome.

PizzaBass is served out of a local’s basement and is amazing.

The locals call it “Roz-land”.

I met more Australians (Brisbane, specifically) than Americans. This despite the mountains location less than 10 miles from the US border.

Mountain Shadow Hostel was nice, but I am too old to stay in a hostel, even when I rent a private room. There was a time…

Immigration officers at land crossings on either side of the border always seem sterner than their airport counterparts. I never get a “Welcome to Canada!” or a “Welcome home!” at a land crossing. He did ask about cannabis products, and when I last visited Canada.

I was worried about the lack of snow in Washington, but the road suddenly climbs to snow immediately after crossing the border.

The swim-through hot springs cave at Ainsworth Hot Springs is awesome and, to my knowledge, unique.

At Kodiak we have a weekly, optional meeting called Lunch & Learn, where somebody in the company talks about something they know well.

Usually the topic is related to, but not strictly a part of, Kodiak and autonomous trucking. And, usually, the format is for the session leader to play a video and add some comments. That’s a lot easier than coming up with an hour-long lecture from scratch.

This week, we learned about silicon chips, including why chips have been in short supply in automotive industry.

The video highlights five areas required for chips:

Instruction Set Architecture

Chip Design

Fabrication

Equipment & Software

Packaging

Of those, fabrication seems like the hardest, due to the massive capital investments required for fabrication equipment.

The whole video is great and worth a watch.

A bonus question somebody asked in our session, that is not addressed by the video: why are silicon wafers round?

Answer: silicon ingots are formed by the Czochralski method, which basically involves melting an ingot and letting it spread out from the center. This results in round wafers.

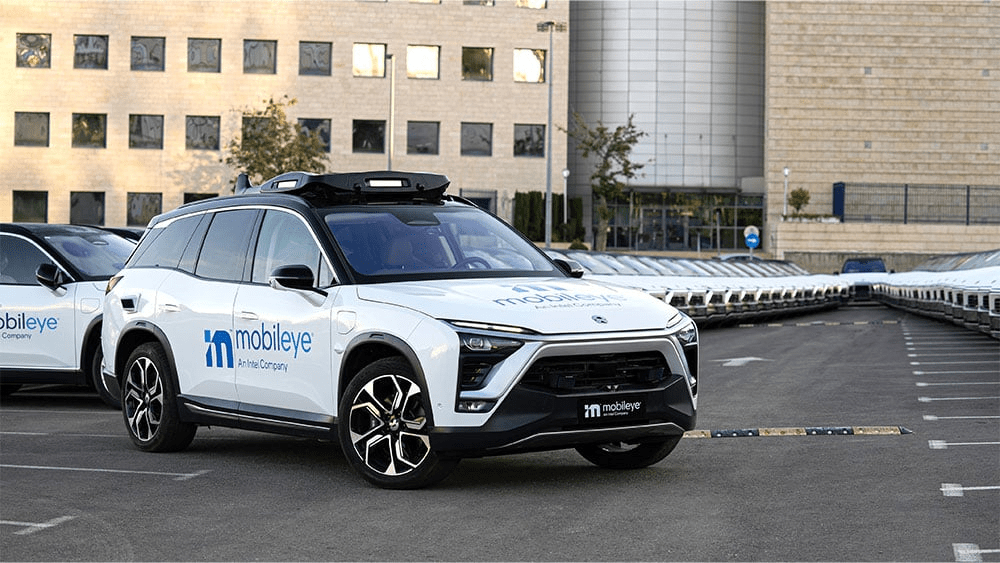

Mobileye is now a public company, under the symbol MBLY.

Perhaps the high water mark of autonomous vehicle funding was Intel’s $15 billion acquisition of Mobileye in 2017. Other transactions were more speculative, like GM’s $600 million acquisition of Cruise, or Uber’s comparable acquisition of Otto, or Ford’s investment in Argo, or Waymo’s multiple outside funding rounds with valuations in the billions and then tens of billions of dollars.

But no single transaction was as big as the Intel acquisition. That one might be bigger than all the other transactions combined.

Five years later, Intel is spinning Mobileye back out, as a public company, at nearly the same valuation as the 2017 purchase price.

This is not a great look for Intel or for the autonomous driving industry, and plays right into a waveofstories about how much cash autonomous driving companies have consumed over the last decade.

But amid all the skepticism, it’s worth looking at Mobileye’s fundamentals. The company has 70% market share in Advanced Driver Assistance Systems (ADAS), with $1.4 billion in revenue, growing something like 30% year-over-year.

That’s a pretty great business. I imagine the market will come around on it.

Aurora has a great blog post up about their upcoming Aurora Horizon service, which will operate with their upcoming self-driving trucks. In particular, the post features a great graphic describing “the middle mile” of autonomous trucking.

“…our customers will drop off and pick up their trailers at our terminals, which are positioned at major freight hubs along our launch lanes, and the Aurora Driver will take care of the long hauls.”

The blog post further describes the inspections and documentation that are required before and after the journey. At the end, Aurora mentions the long-term plan to cover the “first mile” and “last mile”, as well.

“In the future, as we mature our technology, we plan to transition to an end-to-end driver-as-a-service model—where Aurora Driver-powered trucks move customer loads to and from warehouses, and ultimately from distribution centers to stores…”

All of this is subject to change, of course. Since Aurora is a public company the blog post finishes with some boilerplate legalese about the future being unknowable:

“…These statements are based on management’s current assumptions and are neither promises nor guarantees, but involve known and unknown risks, uncertainties and other important factors…”

But as a summary of how an important player in the autonomous trucking industry thinks the business will look in the near future, this blog post is terrific.

We’ve gotten to know many LA neighborhoods, including Downtown and Miracle Mile, Koreatown, Santa Monica, Westwood and West Hollywood, and we’ll begin driving autonomously in several central districts over the coming months as we prepare to serve Angelenos.

The language hedges somewhat – “begin driving autonomously…over the coming months” leaves a lot of ambiguity about how far along this is and to what extent the rides will be monitored by safety operators, versus fully driverless.

The blog post leans in pretty heavily to the continued uniqueness of Waymo’s Phoenix operation:

Waymo remains the only company operating a fully autonomous, commercial ride-hailing service for passengers round the clock in Phoenix’s East Valley – no NDAs, remote operators or pre-defined pick-ups. We’re the first and only company in the world providing autonomous ride-hail trips to and from an airport (Phoenix’s Sky Harbor), and we drive more fully autonomous miles in the U.S. than any other company.

That distinction in Phoenix is huge. Allowing anyone who wants to show up, download an app, and hail the service is a big step up from a limited test audience.

So far, that progress in Phoenix does not seem to have totally translated to San Francisco. In SF, Waymo still seems to be trailing behind Cruise, in terms of number of riders on the service and how ready the company is to go fully driverless. Although data is hard to come by, as both Waymo and Cruise are private companies running limited service in San Francisco.

How well the Phoenix operation translates to Los Angeles remains to be seen.

Kodiak just signed a deal to haul freight for IKEA in our self-driving trucks!

At Forbes, Ed Garsten has a great article situating this latest news in the context of Kodiak’s ever-expanding commercial business, hauling freight coast-to-coast. Kodiak has been on a roll.

One of the overlooked aspects of a big win like this is just how much it says about Kodiak’s ability to work with large multinational corporations. Companies like IKEA take their responsibilities to stakeholders – workers, communities, vendors – seriously. These companies typically have a deep set of partner requirements that new partners like Kodiak must meet. Kodiak’s ability to qualify to carry freight for IKEA speaks volumes about the robustness of our performance.

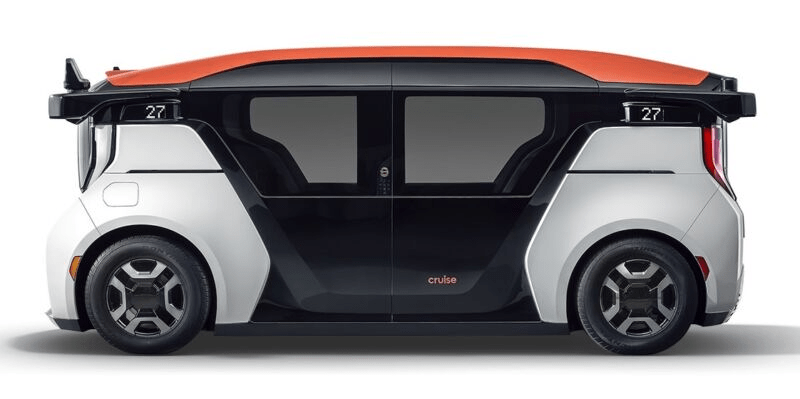

Our purpose-built AV, the Origin, is on track for production! While we eagerly await its arrival for commercial use in the coming months, you may see a human-operated Origin prototype driving on the streets of SF. 👀

I worked on the Origin when I was at Cruise and the vehicle was in pretty early stages. I spent a chilly December week at GM’s Milford Proving Grounds last year, getting the Origin moving autonomously.

If the Origin really is on the road in San Francisco now, or in the near future (the tweet is a little ambiguous), that is awesome progress by Cruise.

The company is on a roll. Eventually, hopefully in 2023, I will be so excited to take my first ride as a paying passenger in the Origin.