Geely, a Chinese automotive manufacturer that also owns Volvo, announced will launch hundreds, and perhaps thousands, of satellites, in order to support V2X and V2V communication.

The launches are a little ways down the road — the current press release touts breaking ground on the facility that will manufacture the satellites.

“Geely Technology Group knows how to start the Lunar New Year right — with important news regarding its future low-orbit exploits. On February 18th 2021, its Taizhou Facility was given its license to begin the commercial manufacturing of its satellites, which will be ultimately used for realizing Vehicle-to-vehicle (V2V) and Vehicle-to X-(V2X) communications to realize full autonomous self-driving.

The license, awarded by China’s National Development and Reform Commission, essentially means that the factory, located in Geely Group’s original hometown of Taizhou in Zhejiang Province, can begin production. When production begins, at present planned for October of this year, the facility will have an estimated production output of over 500 satellites per year.”

In an interesting twist that I hadn’t thought about until now, Geely categorizes these satellites as “new infrastructure.” There’s been a lot of talk in the automotive world about China’s ability to build infrastructure much faster than the US’s, and the advantages that may or may not bring. But I had always assumed this meant infrastructure on the ground. I hadn’t really thought about satellites as “infrastructure.”

The Geely press release is pretty sparse and focuses on V2X communication as the goal, but an article in SpaceNews suggests that the satellites may also foster an alternative and more accureate form of GPS / GNSS. That would make sense, as I typically think of satellites as being useful for receiving data on the ground, but not so much for sending data to the satellite. V2X would require two-way transmission, but navigation systems typically only require one-way reception of data.

GPS has been run more-or-less as an international public service by the US government for decades. Attempts to augment it have typically relied on ground-base supplementary broadcast stations, but those are hard to scale and are easily blocked by hilly terrain. If a private Chinese automotive company controls the next generation of navigation satellites, that would be a big change with potentially big implications.

“Interestingly, the drop in sales only resulted in a temporary inventory backlog. While Manheim estimates that retail used car inventory in April was 161% higher than usual, May used car inventory has dropped 25% below average. The supply reduction may be due to fewer buyers trading in older vehicles, as new vehicle sales followed a similar trajectory from April to May.”

On my way down one of those infamous web-browsing rabbit holes, I stumbled upon an article from the Fall 1988 issue of MIT’s Sloan Management Review, “Triumph of the Lean Production System,” by one John F. Krafcik.

“Really?” I thought to myself. “That John Krafcik?” How many John Krafcik’s can there be in the automotive industry?

Indeed, the article appears to be from the current CEO of Waymo, back when he was in his twenties, a graduate student at MIT.

Krafcik’s first job out of college, before he wrote this article, was at GM’s NUMMI plant in Silicon Valley. The article kind of reads like Krafcik maybe doesn’t think so much of GM — it’s the only company he criticizes by name. (Keep in mind this is 1988, so no aspersions on present leadership.)

Krafcik seems to revere Henry Ford’s production system, and thinks that Japanese lean production is the natural evolution of that system.

Krafcik found that the location of a plant didn’t matter as much as the location of the company’s headquarters. Japenese plants in America were more efficient than American plants in America, and almost as efficient as Japanese plants in Japan.

Krafcik writes that European companies have a strong Not Invented Here bias that has led them to reject lean production, to their detriment.

Product design has a big impact on plant efficiency.

Plant workers should be empowered to improve processes, not just blindly follow instructions.

There’s not really a tradeoff between quality and productivity. High-quality plants can dispose of most inspection and rework processes, which ultimately makes them more productive.

Technology and robots don’t really seem to help make plants more effective.

That last point seems particularly interesting and ironic, given Krafcik’s current role.

It can be hard keeping up with all the different companies working on autonomous vehicles!

I recently came across two lists of autonomous vehicle companies that I found helpful: “The State of the Self-Driving Car Race 2020” (Bloomberg) and “Factbox: Investors Pour Billions Into Automated Delivery Startups” (New York Times).

The Bloomberg article summarizes the larger, better-funded efforts, whereas the Times covers fundraising by smaller startups.

Between the two of them, how many of these companies are you keeping up with?

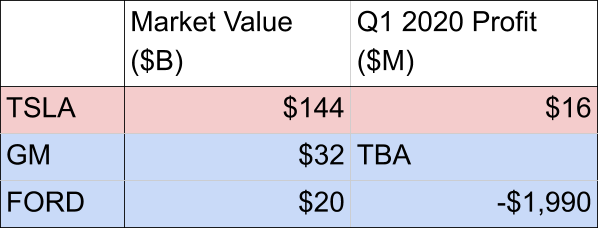

Tesla’s Q1 2020 earnings call was Wednesday. By all accounts, the company crushed it. They turned a $16 million profit, which Car and Driver marks as the first time the company has ever turned a profit in Q1.

The Tesla roller coaster ride has been and up and down for years. The nadir was perhaps when short-sellers baited Elon Musk into tweeting that he would take the company private. That tweet violated all sorts of SEC guidelines and was a bit of a PR disaster. Around the same time, the company periodically came within months or even weeks of bankruptcy.

Flash forward a few years and today Tesla is back on top as the America’s most valuable (and most profitable) care company.

Keep in mind, of course, that by just about any other metric — revenue, units, employees — GM and Ford are an orders of magnitude bigger than Tesla.

But Wall Street seems to think Tesla’s small profit in the present is a prelude to much bigger profits in the future.

Udacity students in attendance on January 17th, you’re invited to lunch!

I am excited to be visiting Detroit next week for the North American International Auto Show. Please come say hello if you’re attending, or send me an email at david.silver@udacity.com.

Here’s the schedule:

Wednesday, January 17, 12:30pm: I’ll be at Automobili-D, speaking on a panel about the autonomous driving industry. Come watch! If you’re a Udacity student, we’ll take you to lunch afterward.

Thursday, January 18, 6pm: RSVP for our Career Workshop and Meetup! We’ll teach you how to present yourself to recruiters in the autonomous vehicle industry, and you’ll practice pitching yourself to other attendees. Also, free food!

Saturday, January 20, 10:30am: I’ll be speaking at the Future Automotive Career Exposition at NAIAS. Introduce yourself to me, then introduce yourself to the many recruiters who will be hiring autonomous vehicle engineers!

Much of the technology that underpins these systems is shared among the industry. A handful of companies like Bosch, Delphi, and Mobileye provide sensors, control units, and even algorithms to car makers, who then integrate and refine those systems.

That claim leaves some wiggle room. Just how much is “much”?

And some of the claim is oversimplified. Whether or not there are “a handful” or somewhat more than a handful of Tier 1 suppliers involved, a lot of that technology is actually flowing through from Tier 2 suppliers. In other words, the Tier 1s are doing a fair bit of “integrating and refining” of their own.

But all this raises more basic questions — who are the suppliers and why do they even exist?

Why The Supply Chain Exists

Few companies produce, distribute, and sell products end-to-end. For example, see Milton Friedman’s famous video about all of the suppliers involved in pencil production.

Many reasons exist for this, including:

Specialization. For example, automotive dealerships usually lack the skills and ability to manufacture vehicles.

Opportunity Cost. An automotive manufacturer might be really good at producing tires, but might decide not to pursue this opportunity because it’s a distraction from the core business of producing cars.

Scale. A lot of effort goes into producing computer chips, and chip manufacturers amortize that cost over all of the chips they sell. Since automobiles use relatively few computer chips, automotive companies don’t have the scale to amortize that cost by themselves.

Regulation. Many US states have laws preventing automotive manufacturers from selling vehicles directly to consumers. Only dealerships can legally sell cars in these states.

The Automotive Supply Chain

Cars are usually either the largest purchase a person makes, or maybe the second-largest, after a house. So it’s not surprising that the automotive supply chain is a little different than supply chains for pencils, or sodas, or basketballs.

Dealerships

Companies that sell vehicles are called dealers. I think of them as physical retail locations, which they often are, but they’re also distinct companies. Sometimes one company will own many dealership locations. The important thing to remember is that these dealerships are distinct and mostly independent from the auto manufacturers.

Dealerships are really good at customer service, understanding the needs of their specific geography and customer base, and vehicle maintenance and repair.

Tesla is trying to disrupt this model, bypass dealerships, and sell cars directly to consumers, but this is the exception, not the rule.

Manufacturers

Automotive manufacturers are the brands that everyone knows — Ford and Toyota and BMW and their competitors.

These firms are commonly referred to OEMs (original equipment manufacturers), which is an unfortunate misnomer. While these manufacturers produce some original equipment, their real strength is in designing cars, marketing cars, ordering the parts from suppliers, and assembling the final product.

The “design” part of that equation becomes a little hazy when it comes to software. Some of the software comes as part of subsystems that are specified by the OEM but built by suppliers. On the other hand, some of the software is built directly by manufacturers.

This is a fuzzy line even in the computer world. Apple and Dell both design computers. But Apple writes its own software (Mac OS, iOS), whereas Dell mostly uses Microsoft Windows software.

Tier 1 Suppliers

Companies that supply parts or systems directly to OEMs are called Tier 1 suppliers. Some of these brands are recognizable, like Bosch or Continental. Some of them are less so.

Tier 1 suppliers specialize in making “automotive-grade” hardware. This means hardware that withstands the motion, temperature, and longevity demands of OEMs.

These suppliers usually work with a variety of car companies, but they’re often tightly coupled with one or two OEMs, and have more of an arms-length relationship with other OEMs. Delphi, for example, was actually owned by General Motors and then spun out as an independent entity.

Tier 2 Suppliers

Many firms supply parts that wind up in cars, even though these firms themselves does not sell directly to OEMs. These firms are called Tier 2 suppliers.

Examples include computer chip manufacturers like Intel or NVIDIA.

Tier 2 suppliers are often experts in their specific domain, but they support a lot of non-automotive customers and so they don’t have the ability or desire to produce automotive-grade parts.

Tier 3 Suppliers

In the automotive industry, the term Tier 3 refers to suppliers of raw, or close-to-raw, materials like metal or plastic.

OEMs, Tier 1, and Tier 2 companies all need raw materials, so the Tier 3s supply all levels. Consequently, the line between a Tier 2 supplier and a Tier 3 supplier that sells into Tier 1s is blurry.

Putting It Together

Consumers shop for cars at dealerships.

Based on what dealerships learn from their customers, they place orders for specific types of cars with auto manufacturers.

Auto manufacturers use the order data to design new cars and source components from Tier 1 suppliers.

Tier 1 suppliers purchase components from Tier 2 suppliers and package it into automotive-grade systems.

Tier 2 suppliers make parts and are happy to sell them to automotive companies, but Tier 2s serve many other industries, too.

Tier 3 suppliers sell the raw materials that other firms in the supply chain require to make their specialized products, systems, and components.

That’s an over-simplified summary, of course.

In reality, consumers are shopping for cars directly on manufacturer websites, and dealerships are discussing after-market parts with Tier 1 suppliers, and Tier 2s are marketing their components directly to OEMs. But the summary above paints a good high-level picture.

Who’s In Control?

Historically, the automotive market has been fragmented, with lots of dealerships, OEMs, and suppliers.

Conversely, software is often a winner-take-most market. Windows is the dominant desktop operating system, Google is the dominant search engine, PowerPoint is the dominant presentation package.

That’s where the Ars Technica article comes in. A lot of people would like to figure out if automotive software is moving to a winner-take-most model, and who that winner will be.

The winner-take-most issue is deep in its own right, and it will take a whole separate post to deal with that. But this supply chain knowledge is kind of a pre-requisite to considering that question.

For now, my short take is that competition is ongoing, it’s not clear if this will be a winner-take-most market, and certainly there’s no clear winner yet.