Reilly Brennan’s Future of Transportation newsletter included links to the pitch decks that Joby and Lucid used in their recent SPACs. In an alternate universe, these would have been the pitch decks presented to growth- and late-stage venture capitalists, and wouldn’t have been available to the public. Because both Joby and Lucid went public via reverse mergers with SPACs, their pitch decks are also public.

The Joby deck has forty beautiful slides and a ton of information. I found it a little hard to parse, though, perhaps because I’m not used to navigating decks of companies at this stage.

I did not a few items:

- Joby plans to start generating revenue in 2024, and to reach “scale” in 2026.

- The pro forma financials call for revenue growth from $0 in 2023 to $2BB+ (!!) in 2026.

- At scale, they anticipate the vehicle to cost $1.3MM.

- The projected returns for investors seem maybe not that great? Again, I found this hard to parse, but I think they hypothesize that if they hit their 2026 goals, and if the stock market applies a 25–30x P/E multiple (!!), then investors today would see a 20% (annual?) return. Lots of caveats.

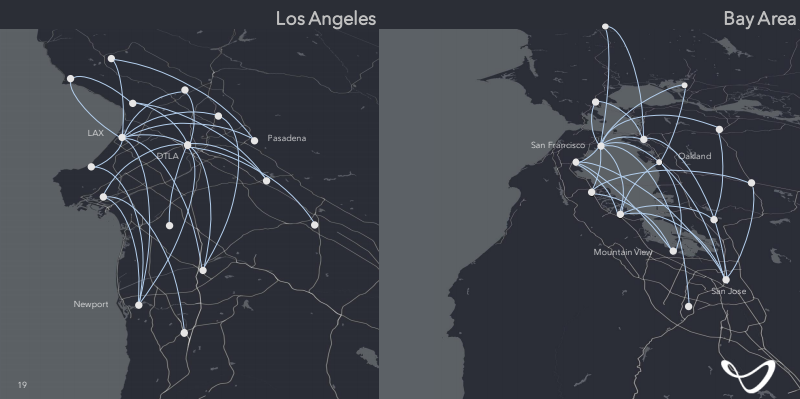

- They forsee a robust market for intra-city transport.

- They will focus on “meaningfully” penetrating each city before moving on to the next, and thus only anticipate penetrating 20 cities in the next ten years.

- They project an average trip length of 24 miles, with an average “passenger load” of 2.3, and a price point of $3 per “seat mile.” Each vehicle will have 4 passenger seats, so the price point per “vehicle mile” is presumably $12. For a hypothetical 24 mile trip, the price would then be $288 total, but potentially as low as $72 per passenger, split four ways. They present this as “cheaper than Uber black for an individual.”