TuSimple is one of the leaders in the autonomous trucking industry. They’re partners with Navistar, one of the leading North American truck manufacturers. And they fly a little bit below the radar, partly because they are based in San Diego, instead of Silicon Valley, and also due to strong Chinese connections that disperses their talent pool across at least two continents.

The startup went public earlier this year, so I spent a bit of time today reviewing both their S-1 and their first 8-K quarterly filing.

Equity

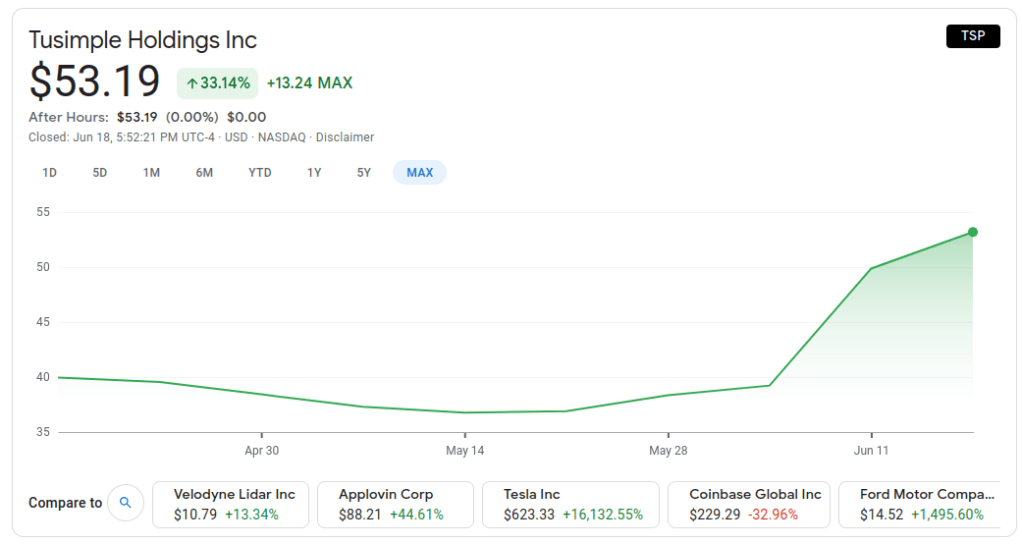

Their stock has performed really well, even in the context of the 2021 bull market.

They’re up 33% in two months as a publicly listed stock, with most of that coming in the past couple of weeks. The run-up seems related to TuSimple’s announcement that they ran a truck overnight across the Southwest and delivered a load of watermelons faster than usual.

I am skeptical how much this one autonomous delivery (with a safety operator in the vehicle) reveals that we didn’t already know. But investors with more money than me seem impressed.

TuSimple’s current market cap is $11 billion, which is pretty stunning for a company with negligible revenue. According to Google Finance, they have 980 employees, which leads to “market capitalization per employee” of about $11 million.

According to their S-1, as of April, 2021, the company had 70 autonomous trucks globally, which had accumulated a total of 2.8 million “road tested miles” (I assume that means “autonomous miles”). Those mileage numbers put TuSimple well behind Waymo, who announced 20 million miles several years ago and has since stopped announcing miles. Yandex and Apollo each announced around 7 million miles this year, albeit for robotaxis, which puts TuSimple on at least the same order of magnitude.

Autonomous Freight Network

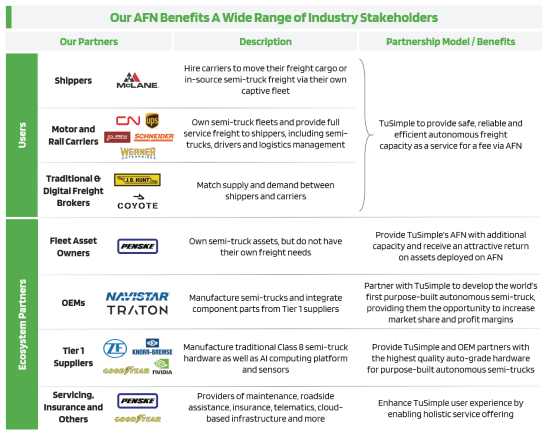

The TuSimple S-1 highlights their Autonomous Freight Network (AFN), which is a nationwide system of mapped roads and highway-adjacent autonomous delivery terminals. AFN allows TuSimple to focus on long-haul transportation, while leaving first- and last-mile delivery to human drivers. This would presumably help with a major obstacle to recruiting truck drivers, which are nights spent away from home and family.

AFN appears to consist of extensive business partnerships, in addition to technology. TuSimple touts partners at many different levels of the logistics chain, including shippers, carriers, brokers, and fleet owners.

Unit Economics

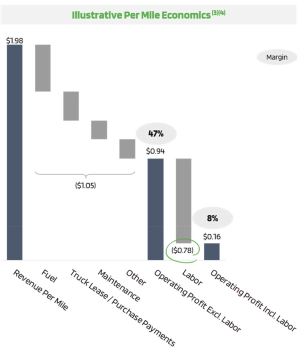

The S-1 contains this nifty break-down of trucking’s unit economics. Trucking generates revenue of ~$2/mile, but about 40% of that goes to “labor” (presumably the driver). After accounting for additional costs, operating margin is about 10%, or ~$0.20.

Interestingly, a meaningful part of AFN and TuSimple’s business model is selling autonomous trucks to companies in the trucking value chain. Those companies will then run their trucks on TuSimple’s network, and pay TuSimple a fee to do so. I’m uncertain under what scenarios it would make sense for a company to purchase a truck and then pay TuSimple to operate it, versus just renting the truck from TuSimple.

S-1

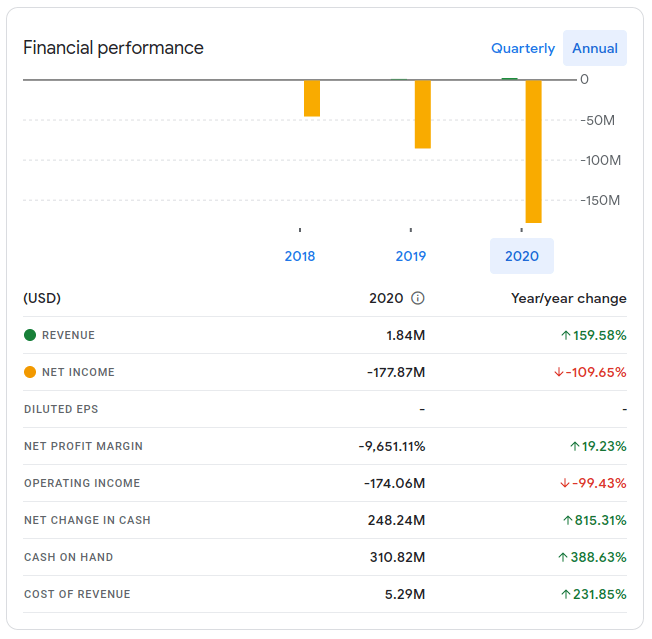

At the time of the S-1, TuSimple had about $300 million of cash in the bank. They burned $100 million of cash in 2020, so they were on pretty-solid financial footing pre-IPO – about 3 years of cash in the bank.

The S-1 projected that the IPO would result in over $1 billion of new cash, leaving TuSimple with about $1.5 billion of post-IPO cash.

Consistent with a solid financial footing, TuSimple has a dual-class share structure, in which the co-founders, Mo Chen and Xiaodi Hou, control the company.

75% of TuSimple’s operating loss due to research & development spending, which makes sense for a pre-revenue autonomous vehicle company.

The company’s leadership is all quite young. Chen and Hou are 36 (or were, at the time of the IPO a couple of months ago). Cheng Lu, the non-founder CEO, is 38.

There’s not a lot of information in the S-1 about Tu-Simple’s geographic distribution, but they do mention that 50 of their autonomous trucks are in the US and 20 are in China. If their employees are similarly distributed (not clear that would be the case, though), then ~700 TuSimple employees would be in the US and ~280 in Beijing, China.

They offer pet insurance to employees.

8-K

TuSimple’s first post-IPO quarterly 8-K filing seems fine. They grew from about 900 employees at IPO to 980, 84% of whom work in research and development.

The IPO raised over $1 billion (!!), as expected.

There’s a photo of Robert Rossi, their new VP of Mapping.

I love their focus on autonomous miles: “There’s No Substitute for Millions of Semi-truck Road Miles.” By the end of Q1 they were up to 3.7 million autonomous miles.

They are in Phase 3 of a four-phase “Driver-Out” program, with the goal of removing the safety driver from the autonomous truck. Phase 1 was design, Phase 2 was prototyping, Phase 3 is expanding the prototype to the fleet, and Phase 4 will be validation. They hope to achieve driver-out by the end of 2021.

They have two trucks in Europe now, in addition to 50 in the US and 20 in China.