Paul Leinert has a fun story in Reuters about an automotive sustainability model developed by Argonne National Labs. The model is called GREET (“The Greenhouse gases, Regulated Emissions, and Energy use in Technologies Model”) and it seeks to capture the environmental total cost of ownership of a vehicle – including production and operation, even taking into account the fuel sources that generate the electricity that goes into electric vehicles.

The model is…not easy to use. I registered with the Argonne website to download it, only to discover that the main model is a .NET program. There is are some Excel-based versions of the model, which I loaded up in Google Sheets. I couldn’t get it to work – there are 18 tabs in the workbook, with lots of cells to complete. All I want to know is whether I should feel virtuous about or ashamed of my 2004 Toyota Highlander.

The Leinert article in Reuters offers some insight. Leinert calculates that a new Tesla Model 3 is more environmentally damaging to produce than a gas-powered vehicle, but the Model 3 is conversely much more environmentally-friendly to operate. More precisely, the Model 3 only becomes more environmentally-friendly than a comparable gas-powered vehicle after 13,500 miles of operation.

“It was up against a gasoline-fueled Toyota Corolla weighing 2,955 pounds with a fuel efficiency of 33 miles per gallon. It was assumed both vehicles would travel 173,151 miles during their lifetimes.

But if the same Tesla was being driven in Norway, which generates almost all its electricity from renewable hydropower, the break-even point would come after just 8,400 miles.

If the electricity to recharge the EV comes entirely from coal, which generates the majority of the power in countries such as China and Poland, you would have to drive 78,700 miles to reach carbon parity with the Corolla, according to the Reuters analysis of data generated by Argonne’s model.”

I’ve heard different off-the-cuff estimates of these numbers before, and I’m happy to see that Argonne put in the labor to make an accurate estimate.

I do wish their model were easier to use.

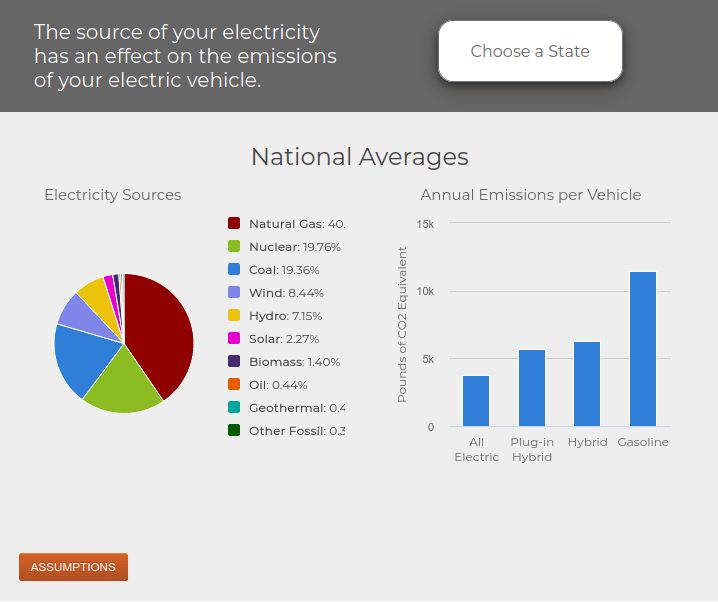

But Argonne does have a nice webpage that tells you how environmentally-friendly it is to drive electric vehicles in different states, based on the power sources for electricity generation.

The requirements, which go into effect ten days from publication (yesterday), mandate vehicle manufacturers (mostly in the case of ADAS) and operators (mostly in the case of ADS) report crashes within 1 day or as a monthly aggregate, depending on severity.

The reporting uses an existing IT system called the Safety Recall Dashboard to fill out a pretty thorough one-page form.

Completing these forms will be a much more laborious task for a vehicle manufacturers than autonomous vehicle operators, simply due to scale. Even the largest autonomous vehicle companies currently have fleets that top out in the low hundreds. Toyota sold over 2 million cars in the US last year.

My initial scan of the form focused on how easy it would be for a large manufacturer to automate the reporting process. Most of the fields appear automatable, possibly with effort. But some, like “Narrative” and “Pre-Crash Movement” seem a lot harder to automate.

I wonder whether this reporting system will become a backdoor to a national automotive collision database. NHTSA limits the requirements’ scope to Level 2 ADAS for the next 3 years, but of course if a Level 2 system collides with a Level 0 vehicle, then the collision will get reported. Eventually, if enough vehicles have Level 2 ADAS, then most collisions will wind up in this system.

The scope could go far beyond evaluating autonomy. Years ago, I was surprised to learn that the national statistics on automotive collisions are quite thin, because so often drivers don’t report collisions to the police or even their insurers. Now vehicle manufacturers are required to report their customers’ collisions to NHTSA.

That could open a real can of worms in terms of privacy and civil liberties. It could also ensure that everyone is safer on the road, most of all vulnerable road users like pedestrians and cyclists.

Cruise co-founder and CTO Kyle Vogt, and Voyage co-founder and CEO, Oliver Cameron.

In my three months working at Cruise, one of my favorite perks has been continuing to work with my friends from Voyage. We’re spread around different teams and even divisions of Cruise – some in prediction, some in planning, some in frameworks, and some of us, like me, in controls. Every few weeks we get together and to exchange notes and laugh and reminisce.

I basically came to Cruise with a built-in network in all different parts of the company. That type of network, in a company as large as Cruise is now, might take a year or more to develop. But from the moment I joined Cruise, if I had a question about perception or embedded systems or remote assistance or any other part of the company, there has always been a former Voyager I could ask.

It’s a secret benefit of an acquisition that delights me 🙂

Add it all up and it should be clear that designing a chip is something very few non-chip companies can really do. Apple Silicon has to cost Apple billions every year, before we even get to working capital for the chips. Even Google has to be carefully weighing which chips it is going to produce.

Consider this strategic risk:

Internal chip capabilities come with big sunk cost issues. The industry is littered with the remains of companies that held themselves hostage to their internal fixed costs – Nokia and its manufacturing plant is just the first to come to mind. Building internal silicon obviously comes with significant financial costs, but companies need to also weigh the cultural and strategic gravity they create.

That is from, “Let’s Build a Chip,” by Dollars to Digits. It’s a terrific explanation (with math!) of both the marginal and average costs of custom chip design and manufacturing.

These days, it seems like every autonomous vehicle company is trying to build a custom chip to keep pace with Tesla. It’s not easy. Or cheap.

I think a lot of labeling and cleaning is outsourced, either to specialty companies, or to specialty teams within a larger ML organization. Perhaps there’s an opportunity for ML engineer to learn more about data labeling and cleaning.

Mat, by the way, now leads the education team at OpenMined.

TuSimple is one of the leaders in the autonomous trucking industry. They’re partners with Navistar, one of the leading North American truck manufacturers. And they fly a little bit below the radar, partly because they are based in San Diego, instead of Silicon Valley, and also due to strong Chinese connections that disperses their talent pool across at least two continents.

The startup went public earlier this year, so I spent a bit of time today reviewing both their S-1 and their first 8-K quarterly filing.

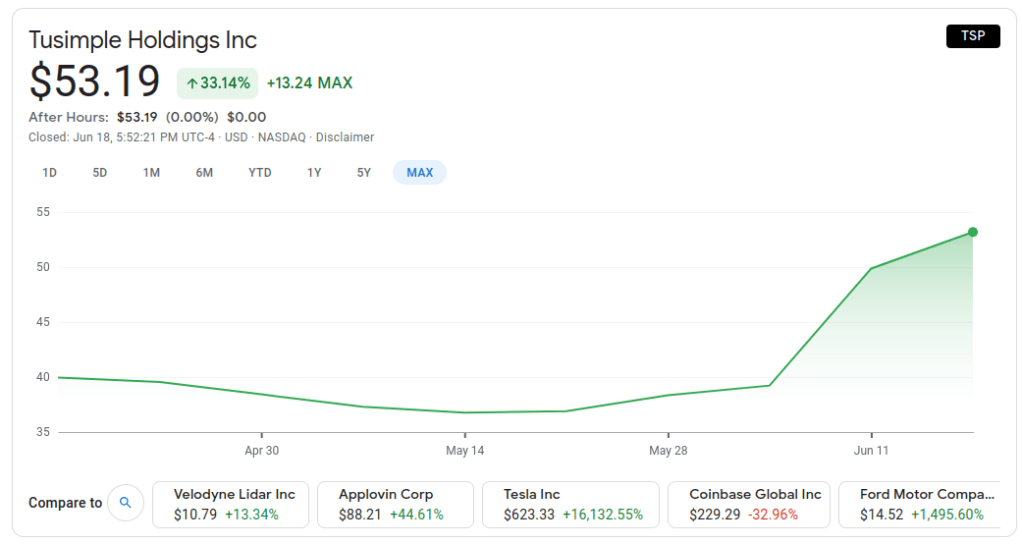

They’re up 33% in two months as a publicly listed stock, with most of that coming in the past couple of weeks. The run-up seems related to TuSimple’s announcement that they ran a truck overnight across the Southwest and delivered a load of watermelons faster than usual.

I am skeptical how much this one autonomous delivery (with a safety operator in the vehicle) reveals that we didn’t already know. But investors with more money than me seem impressed.

TuSimple’s current market cap is $11 billion, which is pretty stunning for a company with negligible revenue. According to Google Finance, they have 980 employees, which leads to “market capitalization per employee” of about $11 million.

According to their S-1, as of April, 2021, the company had 70 autonomous trucks globally, which had accumulated a total of 2.8 million “road tested miles” (I assume that means “autonomous miles”). Those mileage numbers put TuSimple well behind Waymo, who announced 20 million miles several years ago and has since stopped announcing miles. Yandex and Apollo each announced around 7 million miles this year, albeit for robotaxis, which puts TuSimple on at least the same order of magnitude.

Autonomous Freight Network

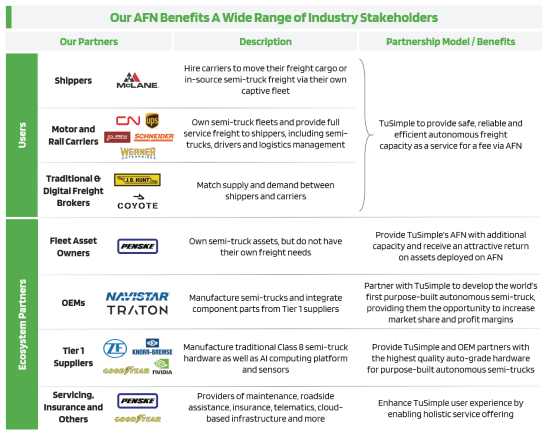

The TuSimple S-1 highlights their Autonomous Freight Network (AFN), which is a nationwide system of mapped roads and highway-adjacent autonomous delivery terminals. AFN allows TuSimple to focus on long-haul transportation, while leaving first- and last-mile delivery to human drivers. This would presumably help with a major obstacle to recruiting truck drivers, which are nights spent away from home and family.

AFN appears to consist of extensive business partnerships, in addition to technology. TuSimple touts partners at many different levels of the logistics chain, including shippers, carriers, brokers, and fleet owners.

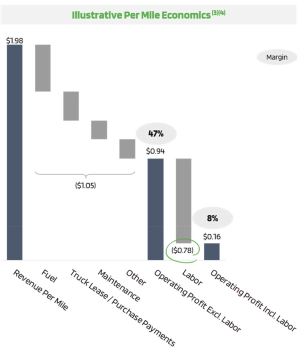

Unit Economics

The S-1 contains this nifty break-down of trucking’s unit economics. Trucking generates revenue of ~$2/mile, but about 40% of that goes to “labor” (presumably the driver). After accounting for additional costs, operating margin is about 10%, or ~$0.20.

Interestingly, a meaningful part of AFN and TuSimple’s business model is selling autonomous trucks to companies in the trucking value chain. Those companies will then run their trucks on TuSimple’s network, and pay TuSimple a fee to do so. I’m uncertain under what scenarios it would make sense for a company to purchase a truck and then pay TuSimple to operate it, versus just renting the truck from TuSimple.

S-1

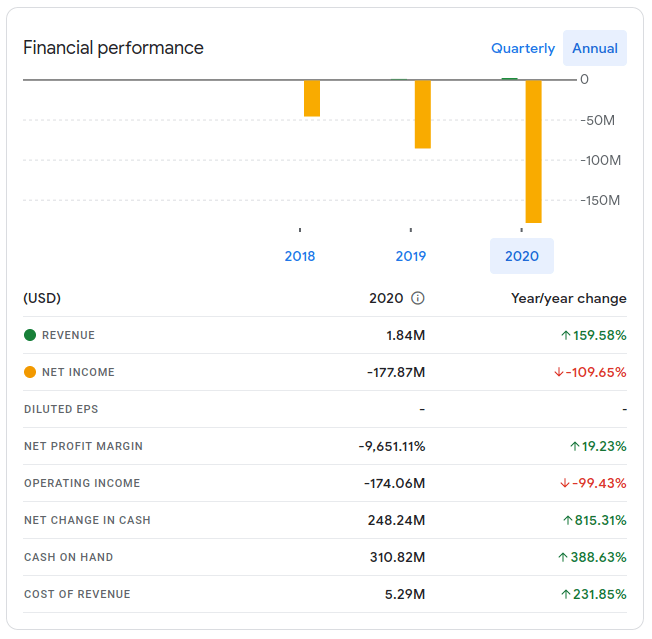

At the time of the S-1, TuSimple had about $300 million of cash in the bank. They burned $100 million of cash in 2020, so they were on pretty-solid financial footing pre-IPO – about 3 years of cash in the bank.

The S-1 projected that the IPO would result in over $1 billion of new cash, leaving TuSimple with about $1.5 billion of post-IPO cash.

Consistent with a solid financial footing, TuSimple has a dual-class share structure, in which the co-founders, Mo Chen and Xiaodi Hou, control the company.

75% of TuSimple’s operating loss due to research & development spending, which makes sense for a pre-revenue autonomous vehicle company.

The company’s leadership is all quite young. Chen and Hou are 36 (or were, at the time of the IPO a couple of months ago). Cheng Lu, the non-founder CEO, is 38.

There’s not a lot of information in the S-1 about Tu-Simple’s geographic distribution, but they do mention that 50 of their autonomous trucks are in the US and 20 are in China. If their employees are similarly distributed (not clear that would be the case, though), then ~700 TuSimple employees would be in the US and ~280 in Beijing, China.

They offer pet insurance to employees.

8-K

TuSimple’s first post-IPO quarterly 8-K filing seems fine. They grew from about 900 employees at IPO to 980, 84% of whom work in research and development.

The IPO raised over $1 billion (!!), as expected.

There’s a photo of Robert Rossi, their new VP of Mapping.

I love their focus on autonomous miles: “There’s No Substitute for Millions of Semi-truck Road Miles.” By the end of Q1 they were up to 3.7 million autonomous miles.

They are in Phase 3 of a four-phase “Driver-Out” program, with the goal of removing the safety driver from the autonomous truck. Phase 1 was design, Phase 2 was prototyping, Phase 3 is expanding the prototype to the fleet, and Phase 4 will be validation. They hope to achieve driver-out by the end of 2021.

They have two trucks in Europe now, in addition to 50 in the US and 20 in China.

Luminar announces a lot of news, to the point that I can’t really tell how impactful any individual announcement is. But Luminar still feels to me like the company best-positioned to offer an alternative to Mobileye in the advanced driver assistance space. Almost every other company in the space is either a specialized sensor or software supplier, or a large integrator, like a Tier 1 supplier.

Luminar seems to have the best combination of comprehensive hardware plus software expertise.

Blade seems like a step in that direction. You could imagine a vehicle manufacturer purchasing Blades without really having to think about how they work. Just design Blades onto the roof and get a perception stack, no problem.

Obviously that’s a naive projection, but that’s the turn-key solution the industry would love.

Waymo, Kodiak, and my own employer, Cruise, all announced fundraising in the last 48 hours.

Waymo announced a monster $2.5 billion funding round, consisting of a wide array of investors:

“Alphabet, Andreessen Horowitz, AutoNation, Canada Pension Plan Investment Board, Fidelity Management & Research Company, Magna International, Mubadala Investment Company, Perry Creek Capital, Silver Lake, funds and accounts advised by T. Rowe Price Associates, Inc., Temasek, and Tiger Global.”

Kodiak announced a seemingly smaller round of investment from Bridgestone, the tire company. Or, more accurately, Bridgestone announced an investment of undisclosed size into Kodiak.

“Bridgestone Americas (Bridgestone) today announced it has made a minority investment in Kodiak Robotics, a leading U.S.-based self-driving trucking company. The partnership will allow Bridgestone to integrate its smart-sensing tire technologies and fleet solutions into Kodiak’s level 4 autonomous trucks.”

Cruise announced a slightly different variant of fundraising, a $5 billion line of credit from GM Financial Financial. We will use the money to build self-driving Origin vehicles, the purpose-designed autonomous vehicle that Cruise and GM are creating together.

“Today we’re announcing that GM Financial, the automotive financing arm of GM, is working with Cruise and providing a $5 billion line of credit so we can efficiently finance the expansion of our fleet as we scale up over the next few years. This bumps up Cruise’s total war chest to over $10 billion as we enter commercialization.”

None of these fundraises mention a valuation. Cruise’s credit line would not normally trigger a valuation change for a privately-held company, and the Cruise News page still lists “$30b+” as the company’s valuation.

Waymo’s valuation has been the subject of a lot of speculation. Prior to this most recent raise, speculation and reporting converged on a $30 billion valuation.

Kodiak’s valuation is probably a couple of orders of magnitude smaller that $30 billion. The Bridgestone investment impresses me, although it’s hard to judge without knowing how big the investment was. In an environment where Waymo and Cruise are working in the tens of billions of dollars, financing a normal-sized startup – a hundred people or so, and a valuation around $100 million or so – is a real challenge.

Sri is a teenage phenom who combines an engaging social media profile with impressive projects on a wide variety of software engineering projects.

I particularly appreciate Sri’s summary of the neural networks in his perception stack. Not only did Sri train a network to detect and classify traffic lights, which is a component of the Capstone, but he also trained MobileNet-SSD to detect cars and pedestrians, which goes above and beyond the requirements.

Several years have now passed since I was part of the team that built this project for Udacity. We had so much fun, and I’m delighted to see that students like Sri are still enjoying it!